I am a new Austrian. That is I was recently given Austrian citizenship and a passport under Section 58c of the Austrian nationality act (2019), which offers dual nationality to descendants of victims of Nazi persecution.

For most of my 68-year life, this was unimaginable. My mother was born in Vienna, and fled in 1939, but turned away from the place that turned away from her. She did not think of herself as Austrian. The United States was her country and California her home. Otherwise only Israel really mattered. She rarely spoke German and never with us.

Mom as a young immigrant

We lived in Asia as children, in India and Singapore, traveling in Malaysia, Indonesia, Thailand, and Japan. . . and then came back through Europe in the 1960’s, where we spent three ill-considered weeks in Austria.

For Mom that was it. She had no further interest, and unlike her friends, she never went to Europe again. The Austrians could not be separated from the Nazis, nor the Poles from anti-Semitism. Dad read European history extensively, trying to make sense of Germany, but I didn’t listen to him.

And as I knew her, an American

Mom did arrange French lessons for me, and I continued in school and into college, before moving to Paris (funded by my parents) in 1972. Mom also taught social discipline, attentiveness. She told us to watch and respect the habits of our hosts. “Your country is judged by your behavior” she said.

With some adjustments, France was a liberation for the son of a European immigrant. I stopped struggling to be like everyone else and knew intuitively how to act. Such was the background to my lifelong relationship with France: an admiration for sophistication–a disdain for the overly material or obvious, a preference for food that tastes.

France became my idea of Europe. It is where my friends were, so I grounded there when traveling to England, Italy, Spain, or Berlin. A history course about Vienna, with Carl Schorske at Princeton, and a class in German (which I barely passed) didn’t hold me. It was France that had my interest. I didn’t think much about Austria, until last year when my sister told me we could apply for Austrian passports. I was surprised and pleased. An EU passport would allow me to spend more time in France.

Sometime in the lengthy application process, my interest changed. My grandfather, a progressive orthodox rabbi’s son, moved from Galicia to Vienna as a teenager and then served in the Austrian army in World War I. My grandmother was as a sheitel macher (a wig maker for Orthodox women), although her own glory was her long blond hair. I am named after her father, who is buried in Vienna’s Central Cemetery, but I have never been there.

My grandparents started a few small businesses and by the late 1930’s owned a couple of small buildings and a workingman’s restaurant (Gasthaus). They spoke German and assimilated, but they were not part of the Viennese bourgeoisie.

I don’t want to kid myself. We are far distant. I hardly knew them and cannot go back to where they left off. But there is something there for me; something I’d like to understand more deeply; a sensibility or an outlook that could feel familiar; something different from France.

So far I’ve not done much; a few history books and German lessons with a language professor in Klagenfurt (south Austria). I’d like a trip to Vienna, when the Covid doors re-open; perhaps a class in history or political science; another doorway to Europe; an understanding of a history and culture that was strikingly influenced by Jews, a closer link to what we purposefully forgot. My sister has used the term reconciliation.

I’d like to follow this road a bit before old age catches up

with me.

Donna Olshan and Emily Chen, at Olshan Realty, have been carefully tracking contracts signed, at $4 million or more, on a weekly and monthly basis since 2011. Contracts are an important measure of current market activity, sales to not usually close for a month or more.

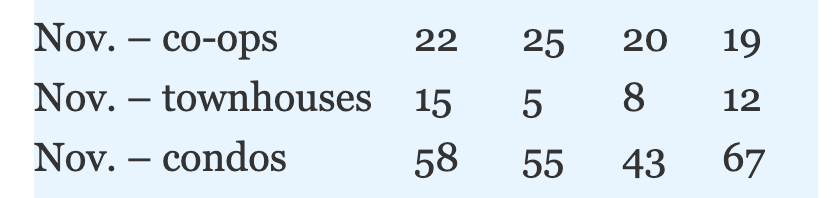

Their monthly findings are summarized in the table below and show that monthly contract volume, for the most expensive apartments and townhouses, collapsed in April 2020. It increased in every subsequent month (although the market was closed to physical showings until late June) but remained well below volume in the prior three years. However, contract volume reached 2019 levels in October, and then stunningly in November it exceeded the number of deals in both November 2019 and November 2018.

As of December 13, 2020, in the prior two weeks, 44 contracts were signed, so the strengthening market continues, perhaps the positive and immediate impact of the election and Covid vaccines.

As is also indicated, condominiums dominate the upper end of Manhattan’s housing market. This is clearly the case in 2020 and the prior 3 years, but certainly would not have been the case when I started in this business some decades ago. Then the upper end was dominated by the cooperative market on Park-Fifth Avenues and Central Park West. More recently, the bulk of luxury listing inventory and contracts is for condos, despite higher prices.

In the Manhattan housing market, sale volume has dropped, but there are deals,

a revival since the market was legally re-opened in late June. This could be in temporary jeopardy this

winter, as we retreat indoors and face a second COVID wave. For

the moment, however, there is strong interest in a listing I have at 33 West 67th

Street, priced at $4,950,000. Three

showings have been scheduled this week, with a possible fourth early next

week.

Broader indicators of price and volume data come from a few sources. Closed sales volume is the most solid, although it lags current market deal-making by a few months. The figures below are from closed sale data on Resource (by RealPlus). Resource combines the data of the Real Estate Board of New York’s Manhattan brokerage firms, and it has a Market Analytics tool that can be used to sort the data according to various criteria.

In these tables, post-Covid-lockdown sale prices and sale volume in 2020 is compared to price and volume data in the same months of 2019. (The real estate market was closed for showings from March 23, 2020 until late June.)

Average sale prices

What the tables indicate is very interesting. There is no consistency in the average monthly prices, both in the market as a whole and for the more expensive properties ($4 million or more). Prices are not likely rising and falling in line with these averages. Monthly averages change all the time, in any market.

Are the monthly average prices lower in 2020? Sometimes yes, sometimes no. But wasn’t the market weaker in 2020? Look specifically at the averages in the $4+ million dollar market; several of them were higher in 2020 than in 2019. This is a very difficult market, so intuitively, yes, prices should be lower this year, but intuition can mislead. The averages depend largely on what apartments sold. Sellers may refuse to sell at a discount, so perhaps only the better apartments are selling; or perhaps a number of high priced new condominiums are closing (following contracts signed a year or two ago); or perhaps the mix of apartments has changed including a higher proportion of larger units. Any, or a combination of these trends impacts the monthly figures and could skew the 2020 averages upwards.

Average sale volume

While the variation in average sale prices has been uneven, the drop-off sale volume has been dramatic. In some months this year, closed sale volume was less than half that in 2019 In others, it was only slightly more than half. However, the slow down actually began prior to the Covid crisis, as indicated by late March, April and May sales. (Sales are generally under contract some months prior to closing.) For sales at or over $4,000,000, the drop off in closed sales volume, relative to 2019, has been much less marked in recent months.

MANHATTAN PRICES, ALL CLOSED SALES

Month

2020, average price

2019, average price

March 23-31

$2,283,870

$1,784,238

April

$2,579,128

$2,068,182

May

$1,801,302

$2,145,735

June

$1,515,294

$3,000,241

July

$2,163,233

$1,629,378

August

$1,997,836

$1,698,525

September

$2,215,970

$1,885,881

October

$1,920,019

$1,690,560

November

$1,768,991

$1,826,103

MANHATTAN SALE PRICES, ALL CLOSED SALES AT/OVER $4 MILLION

Month

2020, average price

2019, average price

March23-31

$8,956,238

$6,588,154

April

$12,528,594

$7,785,631

May

$7,894,099

$8,138,065

June

$6,498,762

$8,424,388

July

$11,000,902

$8,476,618

August

$9,533,866

$8,109,904

September

$10,283,600

$9,267,991

October

$8,087,787

$8,125,232

November

$6,767,558

$9,422,215

MANHATTAN SALE VOLUME, ALL CLOSED SALES

Month

2020 # of sales

2019 # of sales

March 23-31

129

241

April

456

1,077

May

580

1,210

June

770

1,531

July

667

1,017

August

495

1,021

September

514

1,010

October

670

1,028

November

524

821

MANHATTAN SALE VOLUME, ALL CLOSED SALES AT/OVER $4 MILLION

Since the market re-opened at the end of June, I have seen difficulties for both buyers and sellers. On the Upper West Side, an enthusiastic couple negotiated the purchase of a renovated multi-million-dollar apartment, and then backed out in anger (not-negotiation) when faced with relatively-modest improvements. Another client negotiated a very attractive price on an unusual one-bedroom apartment but then changed her mind, after contact with a zealous listing broker, who was trying too hard to pre-qualify her for a difficult co-op board. A third sale hasn’t closed, despite board approval, as the seller’s lawyer struggles to get pay-off information and the stock certificate on a loan that has been sold and is no longer in the portfolio of the issuing lender.

More surprising was a recent board turndown on presumably-liberal West End Avenue. The clients are extremely interesting and accomplished, with liquid assets over four times the contract price in the $3 millions. Their board package was thorough, vetted by me and the listing agents, and with very good reference letters. Yet the board focused entirely on questioning the validity of the husband’s business, a mis-focus that was shockingly inappropriate and arguably illegal in a city that prohibits discrimination based on lawful occupation. As my client rightly complained, there was no one to talk to and no one talked to him.

The co-op system has developed this way, with the support of the courts, hiding behind the filter of closing agents, whose expertise is administrative, and who have no authority. In earlier years, buyers were evaluated on paper; now it is usually on-line. The outcome is the same; buyers can be turned down without explanation, without personal contact and ignoring their references. There are rarely legal and no social consequences. The market is huge; brokers are working all over town. The system is anonymous; board members are free to exercise their social and professional prejudices.

captivating but anonymous

This has long been the case in this large, commercial city, where people don’t know each other and often categorize others without consequence. The issue predates both the internet and Covid 19. But this kind of intolerance is unacceptable, as we struggle to move away from a toxic political environment that thrived on intolerance. It is a waste of human energy in a world with so many bigger problems.

Working from upstate or my apartment in New York, in semi- isolation and driving into the city for the occasional appointment or showing, I manage a tiny piece of Manhattan’s real estate market almost entirely from my laptop. The market has shifted perceptibly in the thirty-five years I have been doing this, from one based on seeing and conversation to one more highly dependent on interpreting the internet and e-mail.

As a young broker, and then as an appraiser, first in San Francisco and after 1985 in New York, I drove or walked from place-to-place, not only to learn the market, but also to develop a taste or an eye for things. Listing information was on printed sheets, in weekly publications, or on cards, so market information was more locally based.

Now there is endless material on-line, much of it accessible to anyone.

There are dozens, even a hundred or more potential listings for each client, photographs, pricing information, old photographs, old pricing information, now videos, and endless commentary, including mine.

Residential real estate, like the retail market, is now increasingly consolidated on the web. Access to information is easier, and getting information requires much less physical movement. But the work is increasingly difficult, as there is now an excess of information, and images, and e-mails. The ease of sourcing and providing information now means that much more information is required, in order to form an opinion, or to make a decision. Superior knowledge is based almost entirely on the ability to sift, recognize, interpret and explain.

There is a disconnect. In the trading of physical things, there is now much less seeing and touching and talking. As a young appraiser, when cooperative prices were not yet recorded, I called and spoke with every broker. As a broker, I previewed property in person. Now in my 60’s, I handle much of this from afar. There are fewer appointments; with images on-line, fewer are needed. Residential real estate is still a local thing, yet I can manage much of it at a distance.

In my own house I also look around less, as I am tethered for hours to the screen or to the phone. I am much more free to move, but I am also more detached from where I am. Real estate work is now much more like that of a writer, with a typewriter or a pen, trading in words, images, and thoughts from my desk.

These are not new trends, but they have been reinforced by Covid 19. Showings are more complex, requiring advance signatures from everyone present. Brokers’ open houses are impossible. Weekend open houses are “by appointment”. For the first time, in July, I brokered the sale of an apartment I had not seen, although we knew the building, and the buyer saw it before bidding. It seemed easy, but only until we assembled the board package by hand, the old fashioned way. And the sale still hasn’t closed, as the seller’s lawyer struggles to get the stock certificate and pay-off information on his client’s loan.

Even with my lap-top, this is a time where getting anything

done is more difficult.

After a break from real estate writing, I remind myself that this work offers the constant pleasure of beautiful things, particularly useful things, like apartments, or houses, or furniture. It is inspiring to see the occasional wonderful house or apartment–there are really very few of them, and it is a pleasure to help find one for others.

Everyone is an audience for housing, and everybody wants something special, each according to his/her or their own sensibilities. I is interesting to think about what makes a place unique or ordinary, what preferences determine its value, and what beauty the market may overlook.

Below, from an apartment for rent in a townhouse on Bank Street.

Thanks for the article you sent me about Sheldon

Adelson and his purchase of the former American embassy residence in Tel Aviv

(le monde.fr).

Your note pushes me to clarify my own view of this situation, as many others have done. But writing this is important for me.

As a Jew, I am fearful of the effects of current struggles on my fellows in Israel and of its humanitarian impacts on the Palestinians and others. However, I live within the safety (until now) and affluence of the United States and have no business dictating a solution to the parties involved. To the degree that I have any direct influence (which I do not), it should be with my own government.

I do not agree with the goals of the settler movement in the West Bank; to me they and their supporters in Israel and the United States are extremist. The notion that God gave us Israel, within its present, or at times larger ancient borders, is self-justifying and self-deluding, except in the general sense, which is that God gives and takes away everything and everybody.

The living conditions of the refugee Palestinians and their lack of prospects are untenable and unacceptable. These circumstances may continue for a very long time, but it is wrong that they should.

That said, if I must choose between defining myself as a

Zionist or an anti-Zionist, then I define myself as the former. I must, although not a religious man, since I

believe that Judaism plays an important role in human affairs, and its survival,

and that of its adherents, is important to me.

It has become common on the left to view Zionism as a European colonial enterprise and the Palestinians as victims of the Israelis. This was actually from good luck or skill born of desperation, since the Israelis might have lost their independence or later wars with the surrounding Arab states, and the present narrative of exploiter/victim would now have been very different. There is also some truth in it, since Zionism in its origins, is a European movement, and most of the early Jewish settlers were European. Or perhaps more precisely, we had lived in Europe, after leaving ancient Israel, for approximately 2,000 years and intermixed, genetically and culturally, with European populations.

But Zionism is the necessity of European antisemitism. However much I love and am fascinated by Europe, our history there was untenable. The refusal of our ancestors to convert to Christianity, and our refusal/and eventual efforts to assimilate, were not acceptable in Europe. The Holocaust was simply the last chapter of 2,000 years of non-acceptance. In the context of 19th century European nationalism, Zionism was survival for a people who no longer had a geographic base.

Our mother and her family escape Europe on the Hamburg-Amerika Line January 1939

Following the Holocaust and the Second World War, it was arguably the only solution, and since we had been largely eradicated in Europe, staying there was no longer safe or plausible, and entry to the United States and other countries was effectively closed.

So many of the survivors came to Israel, and with great difficulty, joining the earlier settlers. The Palestinians feared our arrival in large numbers, eventually resisting the founding of Israel with the support of surrounding Arab states, but they failed. And they failed again. And the victims of this failure, in addition to the Israelis who have died, or who now live in a constantly-militarized state, are the many descendant Palestinians now living in the West Bank, Jordan, Gaza and Lebanon, whose living circumstances are the current focus of attention.

But whose victims really are the Palestinians? Are they the victims of the Jews? Most certainly, since we decided, after centuries of passivity, to protect and secure ourselves, and arguably joined the ranks of the oppressors. Are they the victims of the Arab states, many of whom admitted the most talented and successful Palestinians, but did comparatively little for the remaining refugees (while Israel, post-independence, absorbed approximately 600,000 Jews who were forced out of Islamic countries)? Are they the victims of their own leadership, fragmented, and unable to negotiate realistically, unable to yield? Or are they the also the victims of European antisemitism, and frankly European unwillingness to pay the price of its antisemitism? (Just as we in America refuse to pay for what was done to our native American and black populations.)

When I hear or read criticism of Israel, I am embarrassed and distressed that after two thousand years of reading and thinking and praying in Diaspora, we still define ourselves as Jews by control of a “holy land”, unable now to yield or share it. That the Israelis have been unable and or unwilling to invest in Palestinians and integrate them more fully, and at a higher level, into mutual economic (if not political) interdependence. That we view the Palestinians as inferior or irremediable, instead of simply affirming that we do not wish to be controlled or subjected to them (or anybody else).

Ein Gedi, Israel

But I am also puzzled at those who cannot understand the satisfaction of a Jewish country in our place of origin, who cannot understand the relief of not having to accommodate a Christian or Muslim majority, and who cannot see the necessity of a safe refuge from those who despise, tolerate or fear us. And who do not accept that we are no longer willing to be their victims.

Europe, and not exclusively Germany, has an enormous debt to pay for what has happened in the Middle East. (And of course, Europe and the United States, and generally the West, have other debts to pay.) To every anti-Zionist, may I suggest, as partial solutions, a million dollars–preferably taxed from the rich, but not entirely so–a residence visa and free education for every Palestinian family who would like to resettle in Europe and a serious economic and educational investment in the Palestinian refugee camps. And from the Arab countries, some of whom are very rich, a greater engagement, not only with Israel, which is economically advantageous, but with the Palestinians, to whom they owe a greater interest and a greater obligation.

The plight of the Palestinians is

arguably imperialist and colonialist. But

let us place the responsibility where it lies, in the context of a history that

is still very recent and where there is plenty of blame to share. As both the descendant of victims and the

beneficiary of a privileged life in the United States, I am willing to welcome a Palestinian neighbor

and pay a Palestinian investment tax right now.

Are you?

At this later time in my life, I have a few favored ways to spend leisure time. One of them is sitting in my garden, or on my porch, looking at it. Sometimes, I do nothing but stare. At other times, I share it with friends, over drinks or with long conversations. People visit me at this house, and in the summer the evening light is late. Sitting in the garden is like having another room, or another series of rooms.

I get up, and first thing in the morning, when I come downstairs, I walk outside to look at the plants; the huge purple lilacs, at least 12’ tall, that were here when I moved in; the other lilacs that I added; nine apple trees which we pruned this winter and that flowered last week.

Many afternoons, I spend an hour or so pruning overgrown

shrubs. This morning, before breakfast,

I worked on restoring an overgrown hedge.

The gardener and I cut it back sharply before winter, but it was still

filled with dead branches. It doesn’t

look good yet, and I am learning my way forward, but it now has sunlight in its

center, and there is already new growth from the ground up.

Would it be such a limitation to spend my life visiting

friends, reading books, and taking care of this garden? Is it the need for money or the need for something

else that takes me out of here? Why

isn’t this enough? Why can’t this be

enough for all of us?

The answers are obvious. Not everyone gets to have a garden. Not everyone respects other people’s gardens. Everyone who has one wants to keep it; not everyone is satisfied with the garden they have.

Our father was a very strong man. He was built like a bull, a very good athlete, a boxer, swimmer, and I think a football player in his youth–an excellent and competitive tennis player his entire adult life.

But when I write that he was the strongest person I have ever

met, it means that he said what he thought and argued and fought for what he believed. I wonder if he ever yielded to anyone other than

his wife. Authority, or presumed authority

did not impress or intimidate him. He

was a strong believer in the rights of the underdog and working people and spent

a lot of his time and energy defending them.

He was an engineer and teacher, with an excellent memory, and a great reader, particularly of history

and politics, which he studied closely and cited frequently. He valued the exchange of information and a

good debate.

Dad was intensely loyal. We knew that he had our backs, that we could always count on him. Any crisis brought out the best in him.

He was born in 1921 and so would be nearly 100 now.

I am writing in response to two articles in your paper by different writers, both dated May 12.

Both discuss/report on the impacts of Covid 19 on city real

estate markets, yet they contradict one another.

Carol Galante, in “Now is the Time to Embrace Density”, (https://www.nytimes.com/2020/05/12/opinion/sunday/urban-density-inequality-coronavirus.html) argues that the economic recovery will favor the same cities that prospered before the pandemic, including New York, Seattle, San Francisco and Boston, all driven by innovation, technology and biotech. She refers to a “short-term” reactionary impulse to blame density for the spread of the coronavirus . . . “ And she advocates for less restrictive zoning and less complex and arbitrary building approval processes, permitting and encouraging higher density and more affordable housing.

Matthew Haag’s reporting in “Manhattan Faces a Reckoning if Working from Home Becomes the Norm” questions Ms. Galante’s premise. (https://www.nytimes.com/2020/05/12/nyregion/coronavirus-work-from-home.html) He states that several of the city’s largest and most prominent employers, including Barclays, JP Morgan, Morgan Stanley, Nielson, Facebook, Google and Twitter are now operating with employees at home. The first four have decided that this change may be long-term or permanent. All are reacting to Covid 19, the negative consequences of density, and the realization that they may no longer need corporate offices in order to operate. “Entire economies were molded around the vast flow of people to and from offices . . . “ he writes, yet these economies may no longer be there.

Mr. Haag’s reporting certainly does not support the

near-term revival of downtowns in cities like New York (or San Francisco or

Seattle). Yet the relative demise of our

densest cities, if it does become long term or permanent, can be viewed as an

opportunity to affordable housing advocates like Ms. Galante.

The appeal of our international, gateway cities has been understood as a given over the past generation. The revival of some of our downtowns, including New York since the 1980’s, has been attributed to their architecture, cultural offerings, walkability and mass transit, their appeal to the young “creative class” and thus to their employers. But the revival of these cities has evolved past effectiveness and efficiency because so few of our cities have profited from it. Alongside New York, Boston and San Francisco, which have become unreasonably expensive, are cities such as New Haven, Baltimore, Hartford and Detroit and Providence, that have not profited, or could profit even more. These cities, more specifically their inner cities, now symbolize emptiness, poverty and neglect, which affluent Americans are determined to avoid, but they were once vibrant, and they offer urbanity and density—with affordable historic housing stock, potential development, cultural infrastructure and existing train lines–all at much more reasonable cost than Boston or New York.

Interior view of the Wadworth Atheneum, Hartford, Connecticut by Daderot, January 2016, Wikimedia Commons

The price of expensive housing is not only a burden on the poor, but also on everyone but the very rich. Middle income and even affluent households accept tight, often unattractive apartments, even for millions of dollars in places like Manhattan, as the price of access to good jobs and an interesting city, and in order to avoid a long commute. I know this—I sell and appraise them.

There must be a better way, in a world where urbanity is valued, but where technology makes it functionally unnecessary. I’m not yet sure how, but I am hoping that younger people will look beyond the few favored cities, suburbs, the exurbs, and the countryside, to our older, neglected

George Street, on the East Side of Providence, Rhode Island, February 2017, by Kenneth C. Zirkel, Wikimedia Commons My house in Stamford, New York

cities and even to small towns such as Stamford, New York (where I am presently sheltering from the pandemic, and where large, formerly desirable houses still sell for less than $200,000).

Hopefully employers will take the initiative or follow them. Even public investments, if we can ever afford these again, may occur. It is much cheaper to bring education, jobs, development, affordable housing, and culture to Newburgh, New Haven and Hartford, if Americans are ever willing to do that, than it is to find and develop, buy or rent, additional affordable housing in New York City. Ours is still a large country, with enormous untapped space. Life in many of our neglected, older towns and cities is potentially interesting and humane, and can avoid the very expensive, and at-present, unhealthy, densities of San Francisco and New York.

A New Austrian

I am a new Austrian. That is I was recently given Austrian citizenship and a passport under Section 58c of the Austrian nationality act (2019), which offers dual nationality to descendants of victims of Nazi persecution.

For most of my 68-year life, this was unimaginable. My mother was born in Vienna, and fled in 1939, but turned away from the place that turned away from her. She did not think of herself as Austrian. The United States was her country and California her home. Otherwise only Israel really mattered. She rarely spoke German and never with us.

We lived in Asia as children, in India and Singapore, traveling in Malaysia, Indonesia, Thailand, and Japan. . . and then came back through Europe in the 1960’s, where we spent three ill-considered weeks in Austria.

For Mom that was it. She had no further interest, and unlike her friends, she never went to Europe again. The Austrians could not be separated from the Nazis, nor the Poles from anti-Semitism. Dad read European history extensively, trying to make sense of Germany, but I didn’t listen to him.

Mom did arrange French lessons for me, and I continued in school and into college, before moving to Paris (funded by my parents) in 1972. Mom also taught social discipline, attentiveness. She told us to watch and respect the habits of our hosts. “Your country is judged by your behavior” she said.

With some adjustments, France was a liberation for the son of a European immigrant. I stopped struggling to be like everyone else and knew intuitively how to act. Such was the background to my lifelong relationship with France: an admiration for sophistication–a disdain for the overly material or obvious, a preference for food that tastes.

France became my idea of Europe. It is where my friends were, so I grounded there when traveling to England, Italy, Spain, or Berlin. A history course about Vienna, with Carl Schorske at Princeton, and a class in German (which I barely passed) didn’t hold me. It was France that had my interest. I didn’t think much about Austria, until last year when my sister told me we could apply for Austrian passports. I was surprised and pleased. An EU passport would allow me to spend more time in France.

Sometime in the lengthy application process, my interest changed. My grandfather, a progressive orthodox rabbi’s son, moved from Galicia to Vienna as a teenager and then served in the Austrian army in World War I. My grandmother was as a sheitel macher (a wig maker for Orthodox women), although her own glory was her long blond hair. I am named after her father, who is buried in Vienna’s Central Cemetery, but I have never been there.

My grandparents started a few small businesses and by the late 1930’s owned a couple of small buildings and a workingman’s restaurant (Gasthaus). They spoke German and assimilated, but they were not part of the Viennese bourgeoisie.

I don’t want to kid myself. We are far distant. I hardly knew them and cannot go back to where they left off. But there is something there for me; something I’d like to understand more deeply; a sensibility or an outlook that could feel familiar; something different from France.

So far I’ve not done much; a few history books and German lessons with a language professor in Klagenfurt (south Austria). I’d like a trip to Vienna, when the Covid doors re-open; perhaps a class in history or political science; another doorway to Europe; an understanding of a history and culture that was strikingly influenced by Jews, a closer link to what we purposefully forgot. My sister has used the term reconciliation.

I’d like to follow this road a bit before old age catches up with me.